As the ‘AI disruption of everything’ wreaks havoc on the market, how are the ‘smart money’ players generating alpha? The answer lies in short-term tactical operations.

Smart money on Wall Street achieved significant gains amidst tariff-induced volatility. Market turbulence, driven by sharp tariff fluctuations, concerns over the disruptive impact of artificial intelligence, and brewing conflicts in the Middle East, saw hedge funds and active stock pickers outperform benchmark indices.

Smart money on Wall Street has emerged victorious amidst tariff volatility. Due to sharp tariff fluctuations, negative concerns about the disruptive impact of artificial intelligence, and brewing conflicts in the Middle East, markets have been turbulent. Hedge funds focusing on short-term tactical strategies and active stock pickers outperformed benchmark indices.

The increasingly noisy and restless Wall Street giants, driven by recent market volatility, are accomplishing something that simple index-tracking investments could not achieve over the past few years—making so-called smart money appear exceptionally astute once again.

Amidst market turbulence caused by volatile tariff policies, pessimistic selling due to the ‘AI disruption’ narrative, escalating geopolitical tensions in the Middle East, and overvalued markets, institutional investors such as hedge funds employing short-term tactical operations and quantitative stock-picking strategies rather than long-term fundamental approaches achieved significant ‘alpha excess returns.’ These returns were unattainable through the decade-long buy-and-hold fundamental strategy.

Amidst market turbulence caused by volatile tariff policies, pessimistic selling due to the ‘AI disruption’ narrative, escalating geopolitical tensions in the Middle East, and overvalued markets, institutional investors such as hedge funds employing short-term tactical operations and quantitative stock-picking strategies rather than long-term fundamental approaches achieved significant ‘alpha excess returns.’ These returns were unattainable through the decade-long buy-and-hold fundamental strategy.

Alpha is defined as investment returns significantly exceeding ‘beta returns,’ which refer to synchronous investment gains achieved by tracking benchmark indices. Such synchronized gains from tracking benchmark indices are also known as ‘beta.’

Short-Term Tactical Strategies Triumph! Smart Money Outperforms Indexes in Volatile Markets

This is why global hedge funds, often referred to as ‘smart money,’ have performed exceptionally well. Actively managed short-term tactical institutional investors have outpaced benchmark indices at a level unseen since 2007. Quantitative investment strategies, return-stacking strategies, and risk parity asset allocation approaches—all these smart money strategies have surpassed mainstream benchmarks.

In short, bond yields, credit spreads, and the S&P 500 Index have remained almost stagnant for weeks. However, the situation is entirely different for professional institutional investors who favor short-term tactical trading.

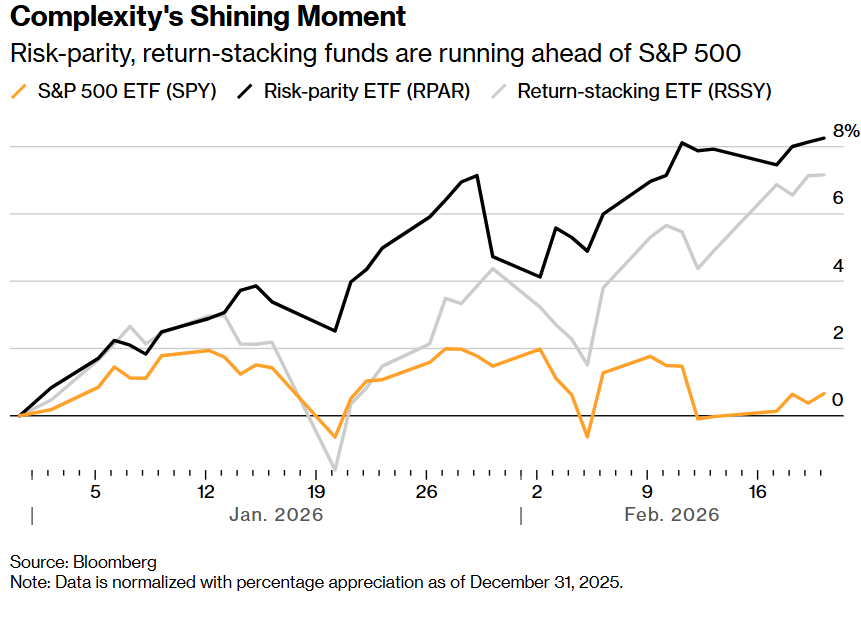

As illustrated above, complexity has taken center stage—risk parity and return-stacking funds have far outperformed the S&P 500 Index.

The market is currently in a state of high instability and multifaceted interference. At the policy level, tariff fluctuations have introduced significant uncertainty; at the technological level, concerns about AI-driven disruptions are pressuring software and growth sectors; geopolitically, escalating tensions in the Middle East are driving volatility in energy and safe-haven assets. Amidst elevated valuations, traditional ‘buy-and-hold’ strategies no longer hold a clear advantage and may even appear sluggish in volatile markets. In stark contrast, short-term tactical allocations and active strategies have significantly outperformed passive index-tracking during this market cycle.

The core factor behind this round of sharp declines in software stocks and sector rotation lies in the pessimistic narrative of ‘AI disrupting everything.’ This narrative swept through global financial markets in mid-February, gaining momentum when Anthropic, known as a key rival to OpenAI, launched a series of AI tools and agent-based collaborative platforms. This triggered a massive sell-off wave across the SaaS subscription software sector and broader software segments of global equity markets. Affected by these severe concerns, the S&P 500 Software & Services Index fell approximately 15% from late January and erased nearly $1 trillion in market value within just one week.

In this round of the market environment, “smart money” strategies such as hedge funds, active stock-picking, quantitative models, and risk parity allocation have performed prominently: the hedge fund index achieved nearly a 3% return in the past month, outperforming the S&P 500 Index by a factor of two and surpassing government and corporate bond indices. Meanwhile, multi-asset quantitative trading strategies and structured products also showed positive returns, with these short-term strategies capturing significant excess returns through techniques like volatility arbitrage, relative value, and trend-following. By contrast, the S&P 500 Index and bond yields have remained range-bound over the long term, leaving passive market strategies “unmoved.”

Market dispersion and concentrated opportunities have emerged against the backdrop of inconsistent releases of macroeconomic and sector-specific risks: software stocks faced sharp sell-offs due to concerns about AI threats, which triggered severe adjustments spreading to insurance, real estate, and traditional labor-intensive sectors. Meanwhile, energy and safe-haven assets like oil prices and gold rose, showing that capital is seeking ways to diversify risk. Additionally, after the U.S. Supreme Court overturned most of the tariff policies, President Trump quickly pledged new tariff plans. While the stock market demonstrated resilience with a rebound, bonds and the U.S. dollar came under pressure, reinforcing directional short-term market volatility.

From an investment strategy perspective, the current market environment is not a long-term haven for passive investing characterized by ‘low volatility and low decision-making costs,’ but rather a mid-term phase featuring ample liquidity, challenging directional judgments, yet presenting ‘tactical opportunities.’ In this context, ordinary ‘market timing predictions’ often backfire, with true excess returns stemming from active short-term trading operations, position management, and rapid responses to short-term event-driven factors.

Diverse sources of market turbulence: AI disruption fears, tariff shifts, and macro risks driving divergence

Their investment strategies are highly diversified and not concentrated in the stock market. The sharp decline in software stocks was primarily driven by market concerns that AI-powered workflow agents like Claude and OpenClaw (formerly Clawdbot, Moltbot) were going viral and threatening to undermine the entire software empire built on SaaS subscription revenue models, triggering rare sell-offs that rapidly spread to insurance, real estate, trucking, and any other industries perceived as labor-intensive business models — sectors believed to be at risk of being completely disrupted by AI. At almost the same time, international oil prices approached their highest levels since August this week after Trump warned Iran to reach a nuclear agreement within two weeks, while the scale of U.S. military deployment in the region reached unprecedented levels since 2003. Gold prices also surged again, breaking through $5,000 per ounce.

Friday brought additional uncertainties. The U.S. Supreme Court overturned most of the global tariffs imposed by the Trump administration — marking his biggest legal setback since returning to the White House. However, within hours, he pledged to impose a new 10% global tariff, stating he would retain existing import tariffs under Section 301 and Section 232 frameworks and hinted at launching more trade investigations. The U.S. stock market remained relatively stable, continuing its AI-driven upward trajectory, while developed-market bonds and the U.S. dollar turned lower. Investors ended the week without respite as Trump considered limited military strikes against Iran.

“Uncertainty at the government policy level is mostly just short-term noise. Will this approach fail? Yes,” said Jim Thorne, chief market strategist at Wellington-Altus. He believes hidden stress signals are evident: a weaker dollar, gold nearing record levels, and investors flocking to value stocks like Walmart, while tech stock valuations remain elevated. “Trump needs to reduce the noise, and investors need to adopt more tactically short-term operations.”

Only seven weeks into the year, the continued outperformance of active stock-picking strategies over passive investments does not inspire confidence among investors. The nature of the market rewarding complex strategies is such that when these strategies are fully understood or take effect, they often reverse sharply before their impact is fully realized. In other words, when market conditions reward complex trading strategies for a period of time, such advantages tend to be short-lived rather than long-term constants. Put differently, once certain changes occur in market conditions, the short-term advantages of these complex strategies may quickly dissipate or reverse, rendering the formerly effective ‘smart money’ tactics ineffective.

Shift in investment paradigm: Short-term investment strategies focusing on complexity and active stock selection become the new relative advantage

However, Jordi Visser, head of AI macro research at 22V Research, sees a deeper context — a disruption driven by AI technology that is making investment increasingly complex. “In a world filled with AI-based atmospheric programming, monthly updates and releases of large AI models, open-source competition from China, and AI agent automation, a five-year competitive moat could be entirely eroded over a weekend.” He wrote in a report. The traditional Wall Street institutional response — waiting for clear trends or situations before reassessing risks — might just be the wrong instinct.

Vise pointed out that the outstanding performance of investments surpassing traditional index-based passive long-term strategies may stem from active trading, position adjustments, and market timing — rather than simply buying and holding an index over the long term. At least for now, sophisticated investors are reaping excess alpha returns.

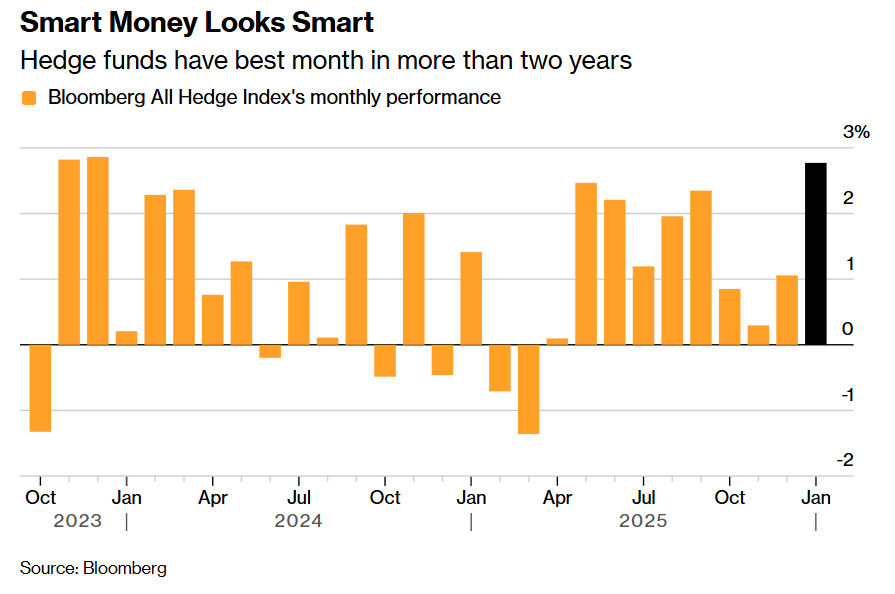

The Bloomberg All Hedge Index, which tracks hedge funds across various sub-sectors including long-short equity, multi-strategy, and distressed debt, grew by nearly 3% last month, marking its best performance in more than two years. This increase was twice the return of the S&P 500 Index and significantly outperformed indices tracking U.S. Treasuries and corporate bonds. The primary drivers were a global influx into commodities (especially precious metals) and highly successful bearish bets — a typical example of tactical positioning succeeding when mainstream indices stagnate.

As shown in the chart above, the current smart money appears even smarter — hedge funds have achieved their best relative monthly performance against the S&P 500 in more than two years.

In the more complex realm of structured products, quant-driven high-frequency trading — typically multi-asset volatility trading designed by large banks for high-net-worth clients and institutional investors, incorporating relative value and trend-following strategies — has risen by an average of 1.1% this year, significantly outperforming the S&P 500 Index. According to data provider Premialab, which tracks approximately 7,000 so-called Quantitative Investment Strategies (QIS), these gains have been notable.

In the exchange-traded fund (ETF) sector, sophisticated tactical strategies have also yielded rewards. An ETF based on volatility-diversified asset allocation, employing a strategy known as risk parity (RPAR), has seen its value rise by nearly 10% this year. Return-stacking funds, which use derivatives to track long-only benchmark indices while investing residual capital in non-correlated trades, have also posted significant gains, with some funds rising by more than 7%.

Meanwhile, stock pickers are finally having their moment to shine after failing to keep pace with the strong AI-driven index rebound. As mega-cap companies linked to data center AI computing infrastructure and software themes retreated amid concerns about overvaluation and AI spending, cautious sentiment in the market has delivered robust returns to active investment funds that avoided exposure to the sector.

The S&P 500 Index, weighed down by persistent sluggishness and sideways movement, is certainly an easier benchmark to outperform. However, predicting how long this rapidly changing environment will persist remains far more challenging, presenting significant opportunities for nimble stock-picking savvy institutional investors.

‘In uncertain conditions, the impulse to adopt tactical maneuvers often leads to poor outcomes,’ said Corey Hoffstein, Chief Investment Officer at Newfound Research. ‘Investors need a portfolio structure that doesn’t require them to predict future movements.’

Despite a holiday-shortened week, U.S. equities still rose, with the S&P 500 Index gaining 1%. For much of the year, the index has been trapped within a 200-point range-bound fluctuation zone, showing minimal progress and stalling at the 7,000-point bull-market momentum threshold. Similarly, the yield on the 10-year U.S. Treasury bond remained range-bound, hovering around 4%, as investors grappled with the upcoming appointment of a new Federal Reserve chair and intense debates surrounding the path of monetary policy.

Although adhering to fundamental-based long-term investment strategies during Trump’s first term brought rich rewards due to robust economic growth prospects, some market participants suggest that the investment paradigm is shifting. Volatile policy swings emanating from the White House — tariff shocks, geopolitical tensions, and fiscal stimulus fluctuations — have altered the baseline assessments of Paul Ticu, head of asset allocation at Calamos Investments.

“This is a moment of regime switch in investment,” he stated. “At some point, policy-level uncertainty and changes will be fully reflected in the market,” he added. “Whether this will result in a sell-off or a rotation trend remains to be seen.”

link

:max_bytes(150000):strip_icc()/GettyImages-1140938075-2e84abc56abe4df09a734dcbd70093f4.jpg "Buffett and Munger’s Top Strategies to Identify Winning Stocks for Long-Term Success")

Insurance Sector: New EIOPA Consultation Clarifying Expectations On National Supervisory Authorities | White & Case LLP")