Africa Gift Card Business and Investment Opportunity Report

Dublin, Feb. 20, 2026 (GLOBE NEWSWIRE) — The “Africa Gift Card Business and Investment Opportunities Databook – 90+ KPIs on Gift Card Market Size, Retail & Corporate Spend, Competitive Landscape, and Consumer Demographics – Q1 2026 Update” report has been added to ResearchAndMarkets.com’s offering.

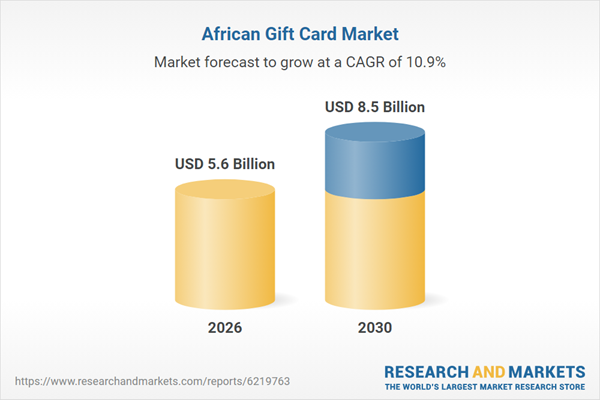

The Gift Card market in Africa is expected to grow by 11.6% on annual basis to reach US$ 5.6 billion in 2026. The gift card market in the region has experienced robust growth during 2021-2025, achieving a CAGR of 12.5%. This upward trajectory is expected to continue, with the market forecast to grow at a CAGR of 10.9% from 2026-2030. By the end of 2030, the Gift Card sector is projected to expand from its 2025 value of USD 5 billion to approximately USD 8.5 billion.

Over the next 2-4 years, competition is expected to intensify around distribution control: Fintech marketplaces expanding cross-border catalogues, large payment networks embedding vouchers into everyday transactions, and South African retailers deepening omnichannel/loyalty mechanics that keep stored value inside their ecosystems. Retail M&A and payments partnerships will matter more than standalone gift-card M&A.

Current State of the Market

- Africa’s gift card landscape is fragmented by country and sits at the intersection of retail gift cards, digital vouchers, and fintech-led prepaid/catalogues. Competitive intensity is highest where modern grocery/retail chains have scaled omnichannel, and fintechs already distribute digital value products through apps and merchant networks, creating overlap between “gift cards” and “vouchers” as functional stored value.

Key Players and New Entrants

- Fintech-led catalogues / digital distribution: Flutterwave Store operates a dedicated gift card marketplace that sells third-party gift cards and voucher codes, competing on availability and delivery speed rather than physical distribution.

- Voucher rails inside payments ecosystems (North Africa): Fawry positions e-vouchers and partner offers within its merchant and consumer ecosystem, competing via distribution reach across its acceptance network

- Retail incumbents (South Africa): Grocery and mass retail players (e.g., Pick n Pay, Shoprite/Checkers) shape closed-loop gift card competition through omnichannel investments and loyalty-linked propositions that influence where stored value is earned and spent.

Recent Launches, Mergers, and Acquisitions

- Deal activity is more visible in adjacent retail/payment infrastructure than in pure-play gift card providers. In South Africa, retailer consolidation (e.g., Pepkor’s acquisition of Retailability brands) expands store footprints that can later be leveraged for gift card and voucher distribution.

- In Egypt, Fawry’s partnerships (e.g., with Orange Egypt and FORSA) reinforce ecosystem scale, improving its ability to bundle vouchers/offers with payments and merchant services.

Anchor Gift Cards to Mobile Money and Everyday Wallet Usage

- Gift cards in Kenya are increasingly distributed and redeemed through mobile money-linked wallets rather than physical cards or standalone gift platforms. Retail and digital-service gift cards are being positioned as stored-value instruments inside existing mobile payment ecosystems, reducing friction in issuance and redemption. Examples include integrations that deliver and redeem digital vouchers and prepaid value through M-Pesa rails, and merchant acceptance via Safaricom-enabled POS and QR flows.

- Mobile money is already the default transaction layer for daily spending, making gift cards an extension of an existing habit rather than a new product. Retailers and digital merchants prefer wallet-based gift cards to avoid the inventory, fraud, and distribution costs associated with physical cards. Employers and SMEs use digital gift cards for incentives and allowances because delivery and reconciliation are simpler through wallets.

- Wallet-native gift cards will become the dominant format for low- to mid-value gifting and incentives. Closed-loop gift cards tied to specific merchants will coexist with wallet-stored value, but distribution will remain wallet-led. Physical gift cards will persist mainly in malls and supermarkets, but will be of declining strategic relevance.

Use Gift Cards to Solve FX and Cross-Border Access Constraints

- In Nigeria, gift cards are increasingly used as substitutes for restricted international payments, particularly for digital services, gaming, streaming, and global e-commerce. Consumers purchase international brand gift cards locally to access foreign merchants without relying on cross-border card authorisation. Platforms such as Flutterwave and Paystack support merchant distribution of digital vouchers and prepaid value as part of broader payment acceptance strategies.

- Ongoing FX controls and intermittent international card spending limits push consumers toward prepaid alternatives. Global digital brands continue to rely on gift cards to maintain access for Nigerian users without direct local acquiring. Informal and SME merchants use gift cards as a workaround for cross-border procurement of software and services.

- Demand for international brand gift cards will remain structurally high, independent of consumer gifting occasions. Regulatory clarity on digital assets and prepaid instruments may formalise this channel rather than replace it. Local platforms will expand aggregation of global gift cards as a payments adjacency, not a retail add-on.

Reposition Gift Cards as Corporate Incentive and Disbursement Tools

- In South Africa, gift cards are increasingly positioned as controlled-spend instruments for corporates, replacing cash bonuses, fuel cards, and paper vouchers. Retailers and financial institutions offer reloadable or multi-merchant gift cards for employee rewards, channel incentives, and social-impact disbursements. Large retailers such as Shoprite Group and Pick n Pay continue to support gift cards across grocery and essential retail categories, reinforcing their use in non-discretionary spend.

- Corporates seek auditability and spend control amid tighter compliance and tax scrutiny. Gift cards reduce cash-handling risk and leakage compared to cash or EFT-based incentives. Retail gift cards align with everyday spend categories, increasing perceived utility among recipients.

- B2B and B2B2C use cases will outpace consumer gifting growth. Multi-merchant and category-restricted gift cards will gain preference over single-brand cards. Banks and payroll providers will more tightly integrate gift cards into corporate payment workflows.

Shift Gift Cards Toward Digital-First Retail and Super-App Ecosystems

- In Egypt, gift cards are increasingly issued and redeemed through digital retail platforms and super-app ecosystems, particularly in food delivery, quick commerce, and online marketplaces. Digital vouchers are used to lock users into specific apps and to circulate value within closed ecosystems. Platforms such as Fawry support widespread digital voucher distribution across online and offline merchants, reinforcing prepaid value usage beyond traditional retail.

- Rapid growth of app-based commerce and digital services creates natural closed-loop environments for gift cards. Consumers prefer digital delivery and instant redemption over physical cards due to convenience and fraud concerns. Merchants use gift cards to retain balances within their platforms and reduce refund outflows.

- Digital-only gift cards will dominate new issuance, while physical cards will become a niche. Super-apps will treat gift cards as tools for balance management and retention rather than as gifting products. Interoperability across platforms will remain limited, reinforcing closed-loop strategies.

A Bundled Offering, Combining the Following 5 Reports, Covering 550+ Tables and 1,400+ Figures for the Gift Card Market

- Africa Gift Card Market Business and Investment Opportunities Databook

- Egypt Gift Card Market Business and Investment Opportunities Databook

- Kenya Gift Card Market Business and Investment Opportunities Databook

- Nigeria Gift Card Market Business and Investment Opportunities Databook

- South Africa Gift Card Market Business and Investment Opportunities Databook

Key Attributes:

| Report Attribute | Details |

| No. of Pages | 1600 |

| Forecast Period | 2026 – 2030 |

| Estimated Market Value (USD) in 2026 | $5.6 Billion |

| Forecasted Market Value (USD) by 2030 | $8.5 Billion |

| Compound Annual Growth Rate | 10.9% |

| Regions Covered | Africa |

Companies Featured

- Addide Stores

- BIM

- Bokku! Mart

- Carrefour Hypermarket (Franchises)

- Carrefour Kenya

- Chandarana Foodplus

- Checkers

- Choppies Kenya

- Dis-Chem Pharmacy

- Eastmatt Supermarkets

- Edgars

- Fathalla

- Game

- Justrite Superstore

- Jumia Nigeria

- Kazyon

- Kheir Zaman

- Khetia’s Supermarket

- Konga

- Magunas Supermarkets

- Market Square

- Metro Market

- MRP

- Naivas Supermarket

- Next Cash & Carry

- Omar Effendi

- Panda Mart / Panda Retail

- Pep

- Pick n Pay

- Prince Ebeano Supermarket

- Quickmart

- RadioShack

- Ragab Sons

- Shoprite

- Shoprite Nigeria

- SPAR

- SPAR Nigeria

- Spinneys

- Uchumi Supermarkets

- Woolworths Food

For more information about this report visit

About ResearchAndMarkets.com

ResearchAndMarkets.com is the world’s leading source for international market research reports and market data. We provide you with the latest data on international and regional markets, key industries, the top companies, new products and the latest trends.

link

Insurance Sector: New EIOPA Consultation Clarifying Expectations On National Supervisory Authorities | White & Case LLP")