Private Markets Outlook 2026: Investing at High Altitude

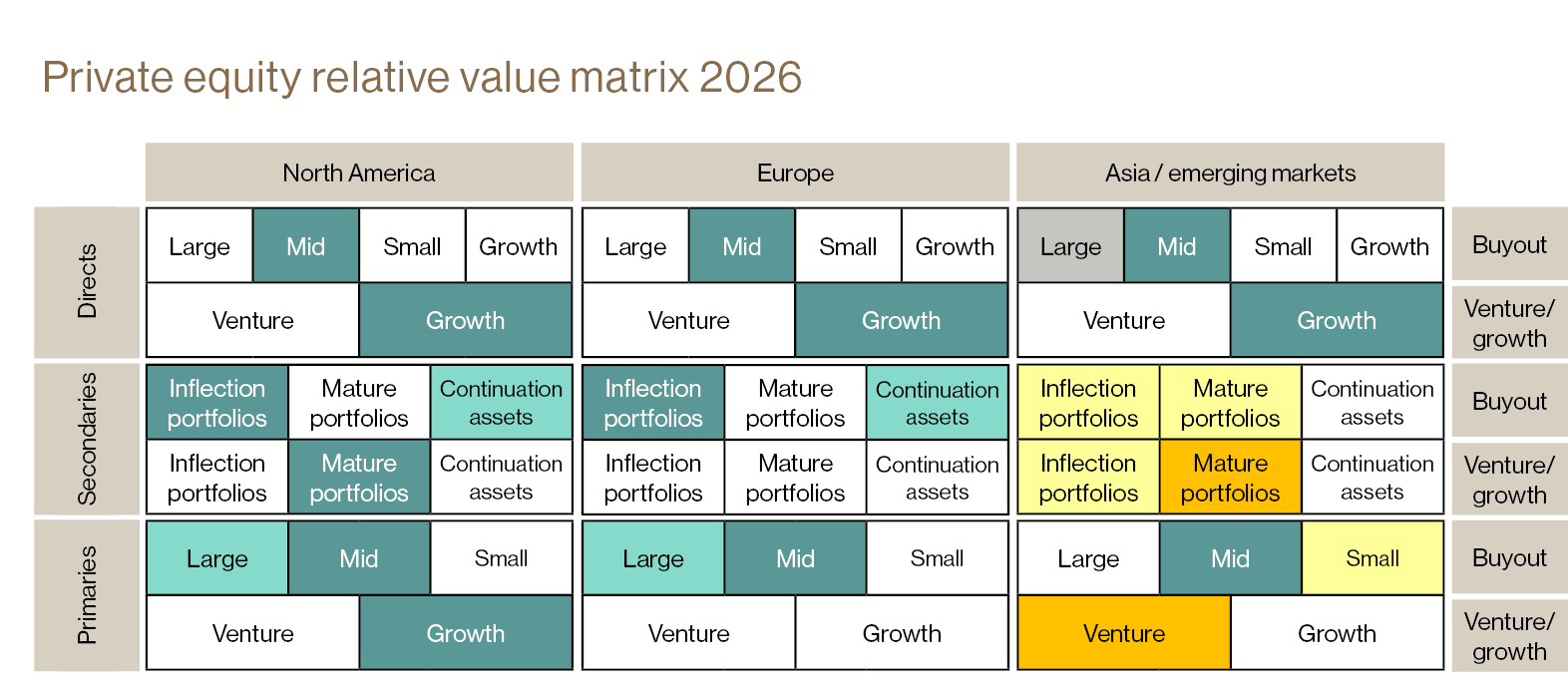

Private Equity

Attractive Flow, Selectivity Critical

Private equity is poised to benefit from a healthy flow of opportunities as transaction activity rebounds from several-year lows. Valuations have been moderating from their 2020-2021 peaks, while the macro backdrop has been supportive. We anticipate this momentum to continue into 2026, particularly in sectors such as pharmaceuticals and goods & products.

Our approach emphasizes control investments to actively steer companies through uncertainty, complemented by thematic investing in resilient structural trends. Opportunistic sourcing remains important to capture dislocations during periods of volatility.

In secondaries, we overweight inflection LP-led transactions given current discounts, while maintaining exposure to mature secondaries as competitors wind down older funds. GP-led continuation vehicles are growing in volume, but quality is uneven; we apply heightened scrutiny. Regionally, both the US and Europe present compelling opportunities.

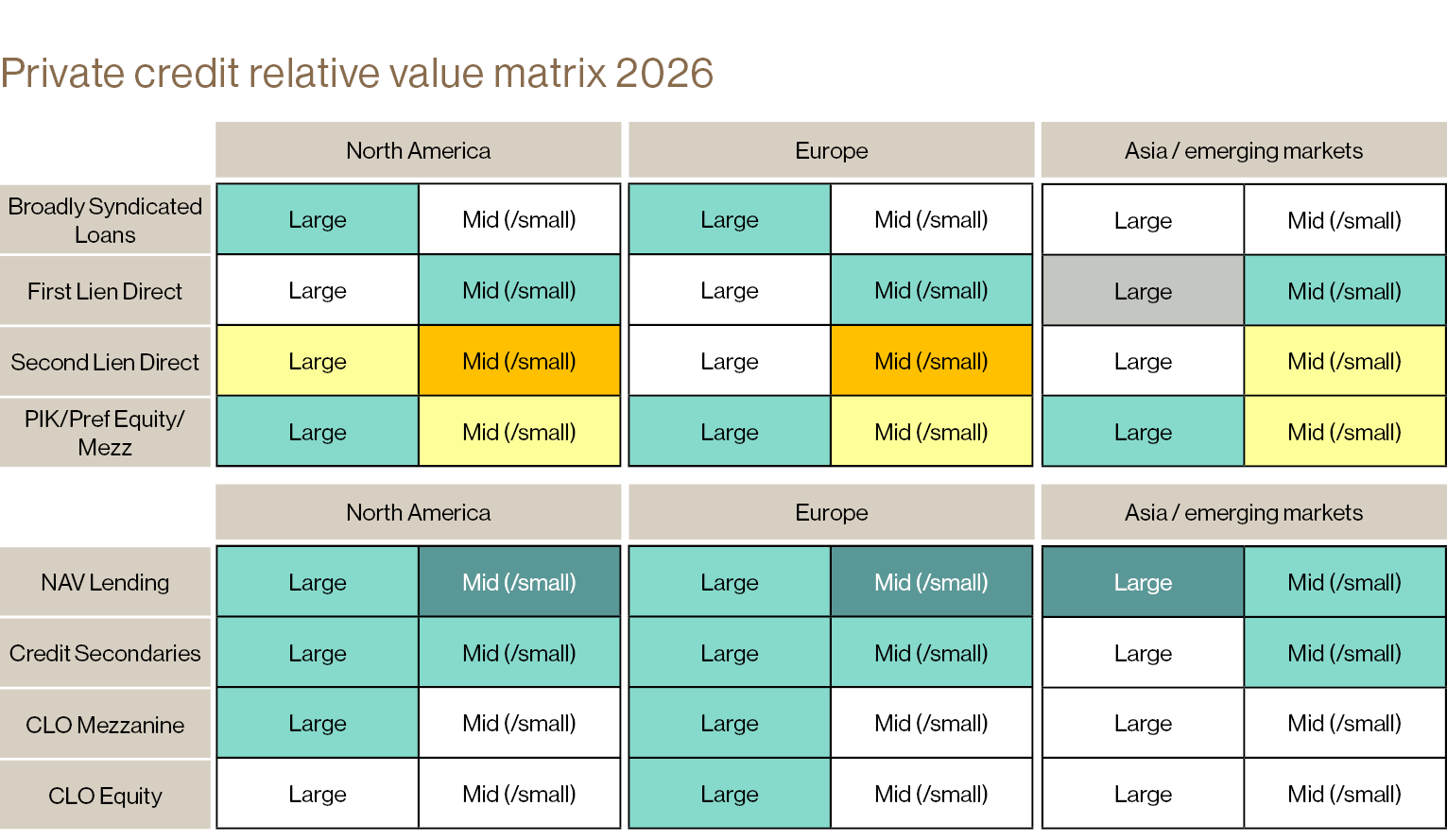

Private Credit

Resilient Profile Amid Moderating Returns

Private credit continues to present a compelling risk return profile despite some moderation in returns as global rate cuts lead to reduced base rates. While deployment and repayment activity remains healthy and steady, returns have moderated as base rates normalized. Overall credit quality remains stable, with leverage levels and default rates relatively low.

Relative value favors Europe over the US, thanks to wider spreads, lower leverage, and stronger creditor protections. We anticipate that bifurcation within the private credit market will intensify: direct lending to large companies may disappoint given margin compression and competitive pressures, whereas highly selective middle-market lending is expected to remain rewarding.

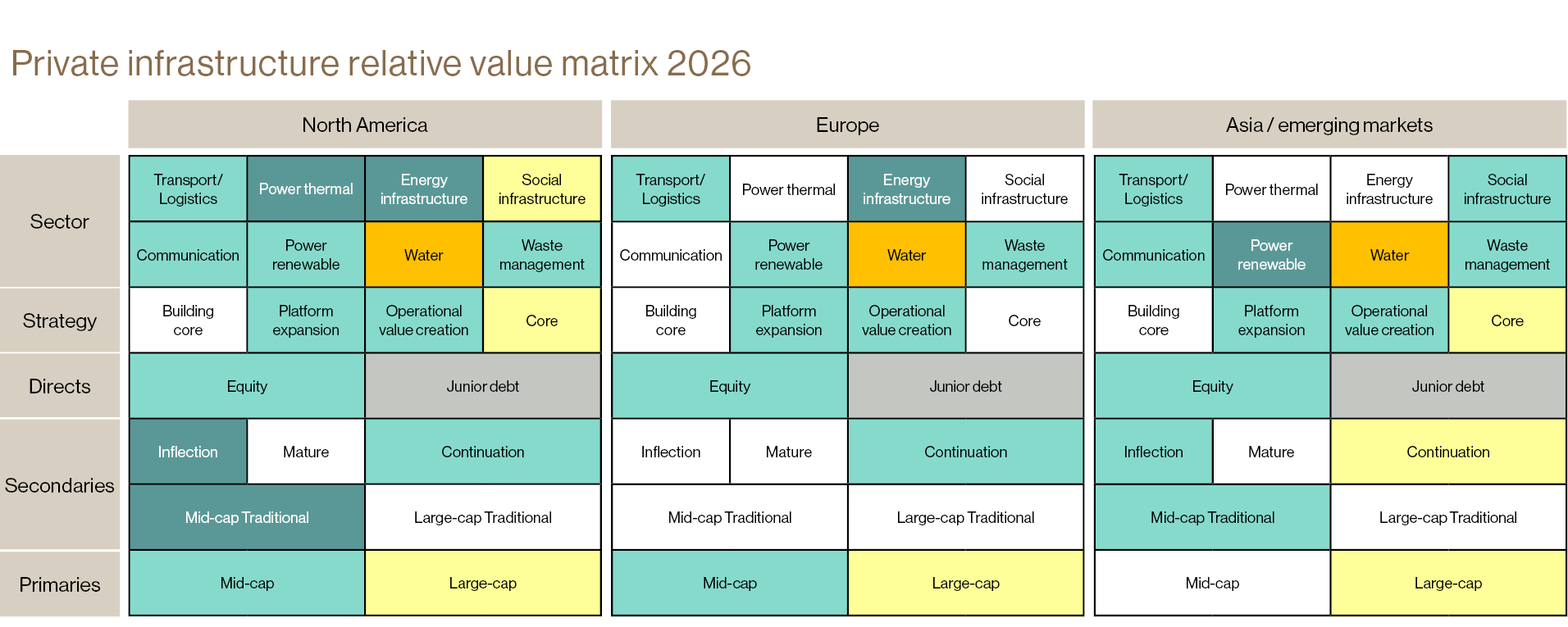

Infrastructure

Overweight for Resilience and Secular Growth

Infrastructure remains a strategic overweight in multi-asset portfolios, offering inflation-linked cash flows and resilience amid potential volatility. Secular trends – including AI-driven data center demand, power generation needs, and modernization cycles – reinforce the asset class’s long-term appeal. Direct infrastructure deployment is focused on selecting the right assets, while secondaries continue to provide stable and predictable flow. We favor mid-market inflection secondaries where discounts remain attractive.

Sector positioning is critical. Power and energy infrastructure in the US remains compelling, while Europe and Asia require selective approaches focused on business model viability beyond government support. It is important to note that additional due diligence may be required in certain sectors, such as renewables and data centers, to carefully assess regional demand and supply dynamics in light of policy changes, shifting priorities, and elevated valuations.

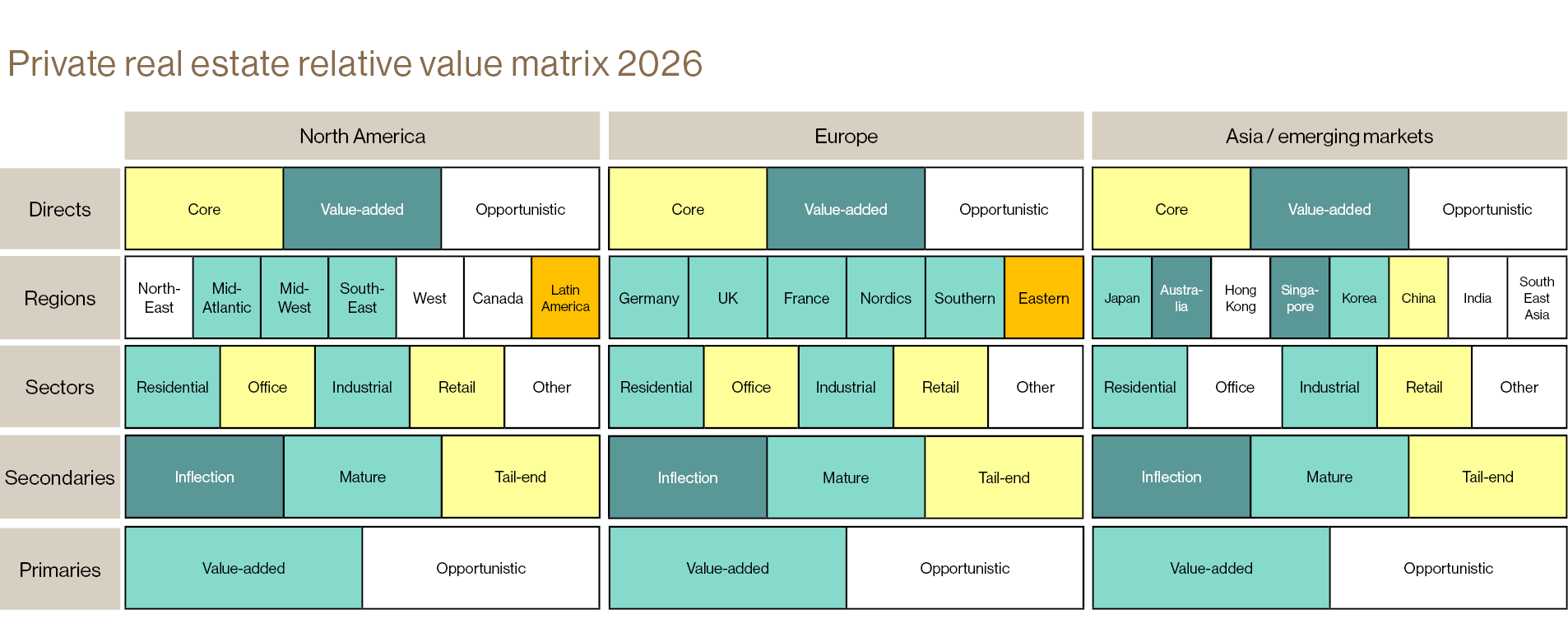

Real Estate

Value-Add Strategies and Regional Selectivity

Real estate investing requires a disciplined focus on value-add strategies, particularly in the US, where high interest rates relative to cap rates have made rent-driven returns challenging. While we anticipate lower interest rates will provide some relief, we maintain that sustainable returns must be anchored in operational value creation. In this context, the adoption of AI and technology continues to emerge as a critical value creation lever across real estate asset classes.

In the US, we maintain an overweight to Sunbelt markets, noting that recent oversupply is being gradually absorbed. In Europe, Southern markets are marginally more attractive than in prior cycles, positioning us as both buyers and sellers depending on market conditions. In Asia-Pacific, Australia and Singapore remain preferred despite competitive bidding from local capital. Across regions, we continue to prioritize residential and industrial assets, closely monitoring local supply-demand imbalances and trends in rental growth. With direct transaction activity remaining muted globally, we see attractive opportunities in secondaries, where good discounts to fair market value can be found.

Royalties

Expanding Market and Portfolio Diversification

We anticipate royalty investing to continue to gain traction as a portfolio diversifier, offering low correlation and resilience through market volatility. The royalty market is estimated at USD 2 trillion and continues to grow. While established sectors such as pharmaceuticals, energy, music and broader entertainment remain core, new areas like sports and technology are emerging, further expanding the opportunity set. (Read our Royalties primer for more.)

For companies looking at funding sources, royalty financing offers a non-dilutive alternative to equity and, unlike traditional credit, does not require debt capacity, making it particularly attractive for businesses seeking flexible capital solutions. 2025 was a pivotal year for Partners Group, marked by the launch of the world’s first cross-sector royalty offering through evergreen structures. Looking ahead to 2026, we anticipate continued expansion of royalty structures and increased lending against royalties.

link

Insurance Sector: New EIOPA Consultation Clarifying Expectations On National Supervisory Authorities | White & Case LLP")