Life insurers’ investment portfolio mix should remain broadly stable, with solid credit quality and core fixed income dominant amid a continued tilt toward private credit and alternative investments, driven by opportunistic repositioning and regulatory reclassifications, according to Fitch Ratings.

The persistent search for yield will continue to drive expansion in private credit across multiple asset classes in 2026, often leveraging the origination platforms of affiliated alternative investment managers.

5 key highlights

- Fitch Ratings expects life insurers’ investment portfolios to stay broadly stable in 2026, with core fixed income still dominant even as allocations to private credit and alternatives continue to creep higher.

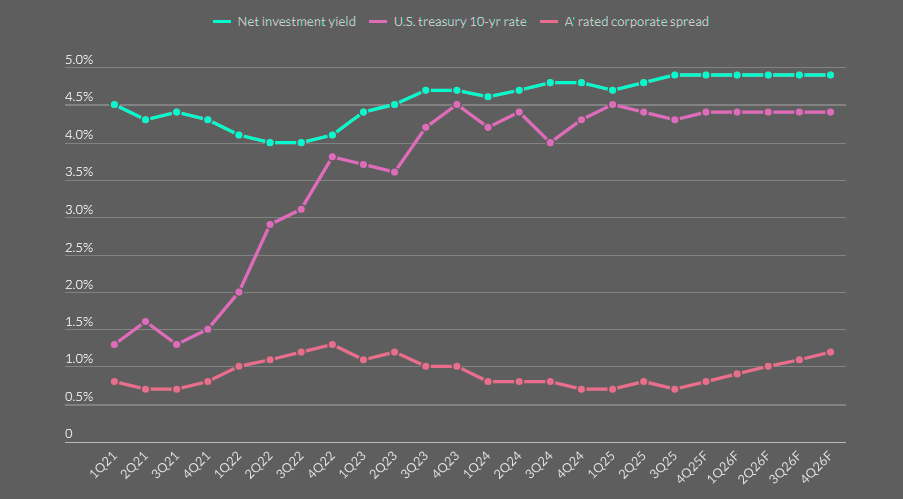

- Fixed-income assets remain the anchor, making up about two-thirds of invested assets, while corporate bonds hold the largest single share at roughly 41%, with only limited shifts in sector exposure.

- Investment risk increases modestly in 2026, but Fitch doesn’t see rising private credit and Level III exposure translating into widespread rating pressure under its base case.

- Commercial real estate, office properties in particular, stays under stress, though higher reserves and improving transaction activity soften the impact on balance sheets.

- Growth in private letter ratings and funding asset-backed notes adds complexity and incremental credit risk, drawing closer regulatory attention rather than immediate balance-sheet strain.

Focus will continue on direct lending, CLOs, private ABS, and private label RMBS, positioning insurers to capture incremental spread while managing duration and liquidity considerations.

We expect investment risk for the industry to increase modestly in 2026 but increased allocations to private credit and Level III assets are not expected result in widespread rating pressure.

Schedule BA assets will also continue to increase, driven by NAIC accounting changes that reclassify certain limited partnership and private fund interests from Schedule D to Schedule BA.

Investment risk for the life insurance industry to increase

Fixed-income assets continued to comprise approximately two-thirds of invested assets at 67% at YE 2024, with corporate bonds maintaining the highest allocation at 41% of invested assets, Beinsure noted.

We expect US life insurers to maintain a broadly stable public and private mix in corporate bonds in 2026, keeping sector concentrations anchored in financials, utilities, and consumer noncyclical, with opportunistic growth in energy exposure.

Fitch expect some opportunistic portfolio repositioning within corporate portfolios. However, insurers are expected to continue to emphasize private placements, given structural protections, while maintaining 144A securities for liquidity (see U.S. Life Insurance & Annuity Sales).

Investments in ABS

Investments in ABS will be more risk-averse in 2026, reflecting ongoing stress in subprime auto and broader consumer headwinds.

Rising 60+ day delinquencies and elevated repossessions are already exceeding levels seen in past recessions, which signals tighter underwriting, wider spreads for weaker collateral, and potentially lower issuance from subprime auto shelves.

Neutral outlook for US life insurers

Fitch Ratings holds a neutral outlook for North American life insurers heading into 2026, even as conditions get tougher.

Strong capital positions, disciplined asset-liability management, and solid liquidity give carriers room to absorb falling policy rates, softer economic growth, heavier macro volatility, and ongoing geopolitical noise.

Operating earnings should stay relatively steady. Net investment income and return on equity get support from rising assets under management, better fixed-income yields, and wider spreads.

That support doesn’t come free. Lower policy rates and choppy equity markets still apply pressure. US life insurers remain sensitive to rate moves, though closely matched assets and liabilities blunt the impact (see about Life Insurers’ Investment Risks).

Fitch outlook and risk view for North American life insurers (2026)

| Area | Fitch assessment |

| Overall outlook | Neutral |

| Capital strength | Strong, provides buffer against volatility |

| Asset-liability management | Disciplined, closely matched |

| Liquidity | Solid across major issuers |

| Credit losses | Modest yoy increase expected |

| Rating pressure | Not expected under base case |

| Severe downturn risk | Not in base case, capital partially insulates |

Fitch expects credit losses to tick up modestly year over year

The agency said it continues to watch investment quality and underwriting closely, looking for late-cycle behavior and risk taking that drifts too far, Beinsure noted.

A sharper market downturn isn’t in the base case. If it shows up anyway, capital strength should cushion balance sheets, at least partially.

Commercial real estate exposure stays a concern, office properties especially. Pressure there hasn’t vanished, but it’s easing as transaction activity picks up and interest rates drift lower.

Life insurers have already built up credit loss reserves. Those buffers reflect the stress in the sector and should cover the expected rise in realized losses.

Investment risk edges higher in 2026

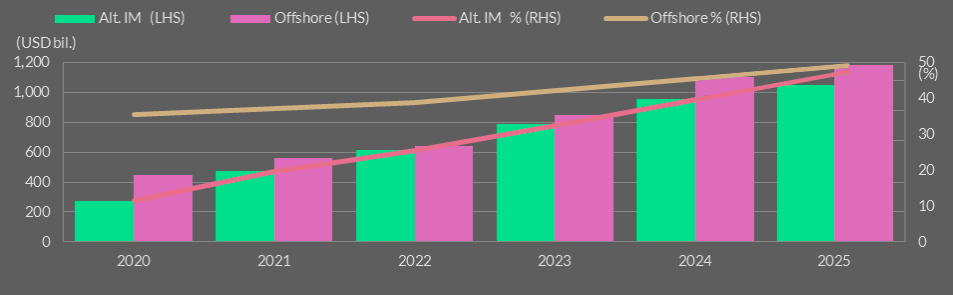

Offshore reinsurance activity continues. Partnerships with alternative investment managers keep expanding.

US life insurers chasing yield and longer-duration returns have increased allocations to private credit and Level III assets. Fitch doesn’t expect broad rating pressure if private credit performance softens over the next 12 to 24 months.

Alternative manager relationships skew strategic. Minority stakes, reinsurance platforms, and sidecars dominate the structure (see Largest Reinsurance Companies in the United States).

Investment portfolio composition and positioning

| Metric | Position |

| Fixed income share | 67% of invested assets |

| Corporate bonds | 41% of invested assets |

| Public vs private credit | Broadly stable mix |

| Sector concentration | Financials, utilities, consumer noncyclical |

| Opportunistic shifts | Energy exposure |

| Preferred instruments | Private placements, selective 144A |

Most large alternative managers already run insurance platforms. That setup limits disruption, even if returns cool.

U.S. Life Insurer Yields and Spreads

The continued shift toward less-liquid investments toward will increase regulatory scrutiny to ensure that the capital held is commensurate with risk.

The focus on private credit will increase, particularly among bank and insurance regulators, given the potential spillover risks from the growing interconnectedness among market participants.

The National Association of Insurance Commissioners in the United States and the Bermuda Monetary Authority have proposed and adopted initiatives, such as strengthening disclosure granularity and capital requirements, to increase transparency and resilience and protect policyholder obligations.

Offshore and Alt. IM Reinsurance Growth

Offshore reinsurance and alternative IM partnerships

| Area | Trend |

| Offshore reinsurance | Growing |

| Motivation | Capital efficiency, earnings support |

| Alt IM partnerships | Expanding |

| Common structures | Minority stakes, sidecars, reinsurance platforms |

| Counterparty risk | Elevated |

| Fitch capital view | Assessed on consolidated Prism basis |

Private credit and alternative investment trends

| Area | 2026 direction |

| Private credit allocation | Expanding |

| Key focus areas | Direct lending, CLOs, private ABS, private-label RMBS |

| Driver | Yield pickup, spread capture |

| Risk impact | Incremental, manageable |

| Rating impact | Limited under current assumptions |

Private ratings and FABNs add risk for US life insurers

The rapid expansion of private letter ratings adds pressure points for US life insurers as portfolios tilt toward assets that are complex, opaque, and largely untested in a full macro downturn.

According to Beinsure, the issue isn’t scale alone. It’s where the capital sits, how liquid it really is, and how values get set when markets turn.

Regulatory follow-through matters here. So does the share of capital tied to PLR-rated issuers. Illiquidity remains a quiet drag.

Valuation practices raise harder questions, especially around governance, subjectivity, reliability, and transparency. None of those resolve cleanly under stress.

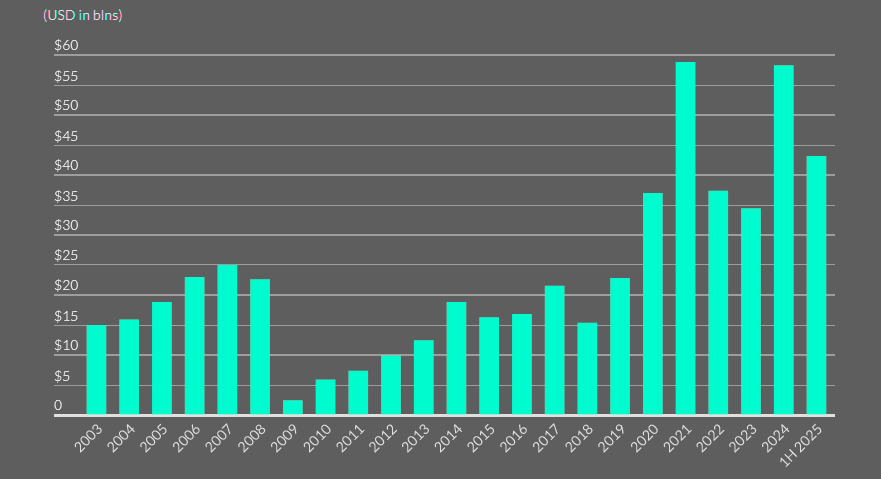

At the same time, favourable market conditions pushed issuance of funding asset-backed notes to record levels. That momentum should carry into 2026, though the pace depends on the timing of rate cuts and how credit spreads behave.

Schedule BA and less-liquid assets

| Item | Trend |

| Schedule BA assets | Increasing |

| Primary driver | NAIC reclassification from Schedule D |

| Asset types | LP interests, private funds |

| Liquidity profile | Lower than traditional fixed income |

| Regulatory attention | Increasing |

Commercial real estate exposure

| CRE segment | Fitch view |

| Office properties | Still under pressure |

| Overall CRE trend | Stress easing |

| Key drivers | Higher transaction activity, lower rates |

| Credit loss reserves | Meaningfully increased |

| Loss absorption | Expected to be adequate |

Private letter ratings (PLRs) – risk watchpoints

| Risk factor | Fitch concern |

| Asset complexity | High |

| Transparency | Limited |

| Stress-test history | Minimal |

| Illiquidity | Persistent |

| Valuation methods | Subjective, governance-sensitive |

| Capital concentration | Key monitoring item |

FABNs come with trade-offs

Their credit sensitivity, rate exposure, and commoditised structure add incremental risk compared with traditional insurance liabilities. When issuance runs hot, even in a generally calm environment, overall credit risk edges higher. Not dramatically. Enough to notice.

Funding asset-backed notes (FABNs)

| Aspect | Assessment |

| Issuance volume | Record levels |

| Market support | Strong issuer and investor demand |

| 2026 outlook | Continued growth |

| Sensitivities | Credit spreads, rate cuts |

| Risk vs traditional liabilities | Higher |

| Impact at scale | Marginal increase in credit risk |

U.S. Life Insurer FABN Issuance

Fitch expect offshore (re)insurance activity to continue growing in 2026 as insurers seek to increase reported capital and earnings via spread-based transactions. This can elevate counterparty credit risk.

Fitch evaluates reported capital using the Prism capital model on a consolidated basis, which limits the scope for regulatory arbitrage to affect assessed capital strength and credit profiles.

FAQ

Fitch maintains a neutral outlook. Capital strength, disciplined asset-liability management, and liquidity give insurers room to handle rate cuts, slower growth, market volatility, and geopolitical risk

Not in a dramatic way. Fitch expects portfolios to remain broadly stable, with fixed income still dominant, even as insurers continue a gradual shift toward private credit and alternative assets.

The search for yield hasn’t eased. Insurers keep adding private credit across asset classes, often using origination platforms linked to alternative investment managers to pick up incremental spread.

Fitch doesn’t expect broad rating pressure, even if private credit performance weakens over the next 12 to 24 months. Capital buffers and portfolio diversification provide insulation, for now.

Schedule BA exposure continues to grow, partly due to NAIC accounting changes that reclassify certain private funds. These assets tend to be less liquid, which nudges overall investment risk higher.

PLRs sit on assets that are complex and opaque, with limited stress-test history. Fitch flags concerns around concentration, illiquidity, and valuation practices that rely heavily on judgment.

Scrutiny is increasing. In the US, the National Association of Insurance Commissioners and the Bermuda Monetary Authority are tightening disclosure and capital rules to ensure capital levels keep pace with embedded risk, especially in private credit and offshore reinsurance structures.

………………

AUTHORS: Jamie Tucker – CPA, CFA, Senior Director, Life Insurance Fitch Ratings, Laura Kaster – CFA, Senior Director, Fitch Wire (North and South American Financial Institutions)

Edited by Yana Keller – Insurance Editor at Beinsure Media

link